In an earlier article, Nigerian payment system operators were explored. Who they are, their roles in the Nigerian financial system driving financial inclusion, and how to get started as one. This article focuses on Ghana.

Ghana is a country in West Africa with an estimated population of 29.6 million (2018) according to the World Bank. The Bank of Ghana (BoG) is the central bank of Ghana, responsible for developing financial inclusion in Ghana. BoG also occupies a unique and important role in Ghana’s payment system, overseeing, operating, and participating in the payment system. The other participants are commercial banks, service providers, and users like the banking public. Commercial banks and service providers will be looked at in this article.

Commercial Banks

Commercial banks are financial institutions with the primary functions of receiving deposits, dispensing these deposits back when needed, and providing loans to individuals and businesses. There are 23 banks in Ghana, operating on a universal banking model. BoG replaced the three pillar banking model – commercial, merchant, and development, with the current universal model in 2003. Access Bank, Ecobank, Absa Bank, Bank of Africa, and Zenith Bank are examples of banks in Ghana.

To get a banking license in Ghana, these are the steps to take.

1. Write an application to the BoG, applying to be given permission to carry on the business of banking.

2. Indicate in the application what type of banking license you are seeking. There are currently 9 categories of banking license in Ghana. So you have to identify the license you are seeking. For example, class one banking license. This license is for universal banks i.e. all traditional banks in Ghana.

3. Attach to the application:

- A true copy of the Regulations.

- Details like names, occupations, and addresses of significant shareholdings.

- Feasibility reports of the proposed bank including a business plan and the first five years financial projections.

- Director’s particulars. Directors concerned with managing the banking business.

- Documented evidence of the business capital, the sources of this capital, and other sources of funds.

4. Final approval and licensing by the BoG.

Service Providers

According to the Bank of Ghana, service providers are the printers of payment instruments and telecommunication companies that provide for the payment system, infrastructural arrangements.

Mobile Network Operators

Mobile banking was introduced in Ghana in 2009, but was not successful in gaining the traction other African countries had. The reason for this was BoG’s restrictive Branchless Banking Guidelines. When the BoG revised the guidelines in 2014, releasing new agent and e-money guidelines, the success of Ghana’s mobile banking began. Mobile network operators were permitted by the new regulations to own and operate, under BoG’s supervision, mobile money services. Mobile money services include bill payments, Peer-to-Peer (P2P) money transfers (money transfer from one person to another), and payments of salary.

What followed was MTN, the telecommunications giant, invested heavily in creating awareness and educating customers, as well as recruiting agents and merchants.

This year, the Bank of Ghana published data that showed that there are now 235,000 active agents in Ghana and 14.7 million active mobile money accounts, roughly half the population of Ghana.

Examples of mobile network operators involved in Ghana’s mobile banking are MTN, Vodafone and AirtelTigo.

Mobile network operators involved in mobile banking are classified as non-bank entities providing electronic money services or engaged solely in the business of e-money and activities related or incidental to the business of e-money, under the regulation and supervision of the Bank of Ghana.

The minimum capital requirement for mobile money operators is 20 million Ghanaian cedi ($3.4 million) and PSP (Payment Service Providers) Electronic Money Issuer is the license type required for mobile money operators.

Agents

There are varying requirements to become an agent in Ghana, depending on the bank or mobile network operator the agent wants to work with. The requirements to become an agent for MTN include owning a registered business, filling and submitting a form known as agent recruitment form, filling and submitting a form known as agent account handler form, and meeting the minimum merchant/agent code of ethics requirements.

Agents in Ghana have their own mobile money agent stalls, branded with the logo and colors of their telecom partner. In 2015, the ratio of MTN stalls like this, outnumbered bank branches by a factor of almost 20:1, according to data by the Bank of Ghana. Mobile money agent stalls provide financial services like cash depositing and withdrawals.

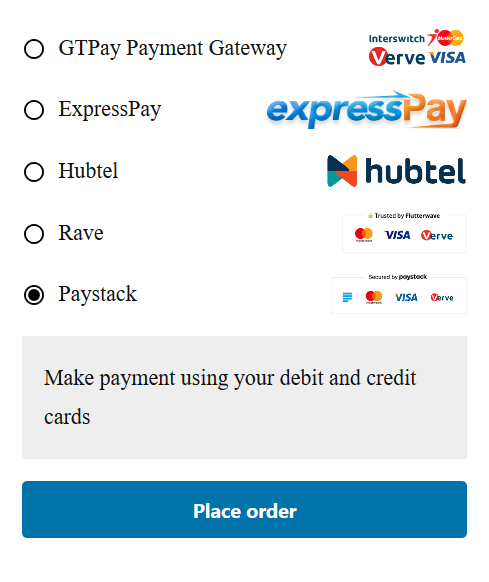

Payment Gateways

Payment gateway companies’ process, using credit or debit cards, online payments for e-commerce businesses, mobile/computer applications, and the traditional brick and mortar stores. Examples of payment gateway companies in Ghana are Flutterwave, Paystack, ExpressPay, and iPay.

The enactment of the Payment Systems and Services Act, 2019, by the Bank of Ghana, was a needed regulatory reaction to the emergency of fintech companies like the ones that offer payment gateway services. The act provided the requirements for Payment Service Providers (PSP) to get licensed and authorized.

The licensing requirements depend on the license type. For instance, PSP Electronic Money Issuer require, with a 5-year tenor, a capital of 20 million Ghanaian cedi ($3.4 million) and a license/renewal fee of 25,000/100,000/10,000 Ghanaian cedi ($4200/$17000/$1700).

The license required for payment gateways is PSP (Medium License) with a tenor of 5 years, a license/renewal fee of 8000/15,000/5000 Ghanaian cedi ($1300/$2500/$850) and a capital requirement of 800,000 Ghanaian cedi ($136.5 thousand)

Payment Switch

Ghana has a national switch called gh-linkTM, installed by Ghana Interbank Payment and Settlement System (GhIPSS) in 2012. The gh-linkTM is an interbank switching and settlement system that allows banks, other financial institutions, and switches to share each other’s ATMs (Automated Teller Machines) and POS (Point of Sales).

The gh-linkTM interconnects the switches of financial institutions and systems of third party institutions to enable them to use a common platform for inter-bank transactions in an efficient and effective manner.

ATM Operators

An ATM dispenses cash and performs other banking services to regular people as long as they insert a credit/debit card into the machine. The entity who is in charge of an ATM’s operations is called an ATM operator. According to a 2018 data from the global economy, Ghana has 11.65 ATMs per 100,000 adults. This is below the world’s average of 53.37 ATMs per 100,000 adults.

The provision of ATM services in Ghana are limited to banks and consortiums of banks and other corporate bodies, according to BoG’s guidelines for operating ATMs and POS systems in Ghana.

Microfinance Banks

There are three tiers of licenses that can be applied for to become a microfinance bank in Ghana. Tier 2, Tier 3, and Tier 4. Tier 2 and Tier 3 companies are microfinance and money lending companies that require a minimum paid capital of 2 million Ghanaian cedi ($341,000). Tier 4 licensing is for Susu collectors (people trusted with low income earners daily deposits) or moneylenders, both which can be individuals or enterprises. However, the individual or enterprise must be a member or an affiliate with the umbrella association for Susu collectors or moneylenders before getting licensed, subject to application processing and licensing fees.

Before applying for a license, the entity must be a body corporate incorporated in Ghana. Then an interview follows. Application, approval in principle, and final licensing are the next and final steps in becoming a microfinance bank in Ghana.

{kind=link}