What happened?

Silicon Valley Bank collapsed with astounding speed on Friday. Investors are now on edge about whether its demise could spark a broader banking meltdown. On the markets, the panic movement started after Silicon Valley Bank (SVB) announced that it was seeking to raise capital quickly to cope with the massive withdrawals of its customers, without succeeding and having sold its financial securities for $21 billion (€19.7 billion), losing $1.8 billion (€1.7 billion) in the process.

Why did it happen?

Investors were surprised by the news, and it made them worry again about the banking sector's health. This is especially true given the rapid rise in interest rates, which is lowering the value of bonds in their portfolios and making it more expensive to get credit.

What are the regulators doing?

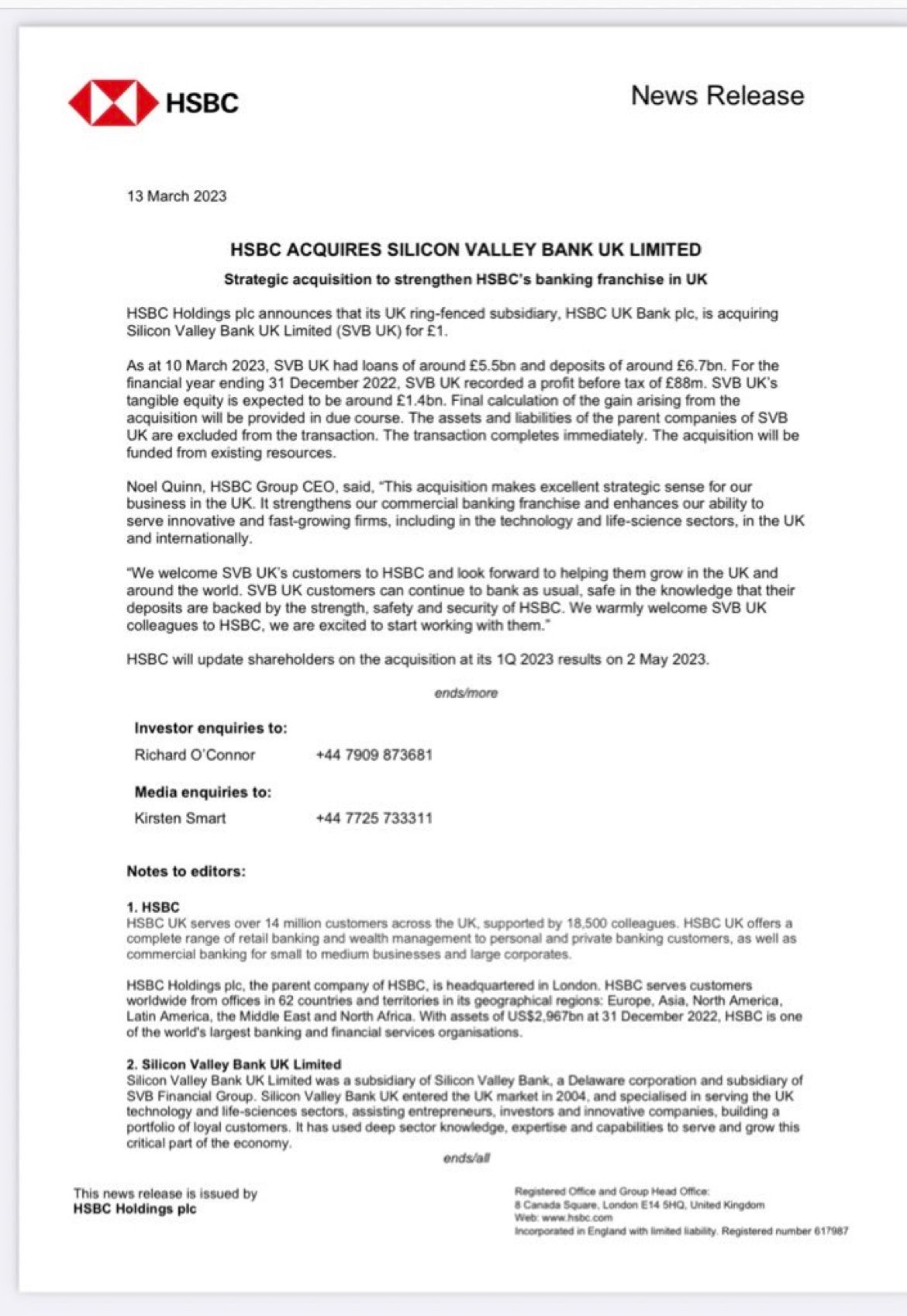

The US Federal Reserve has bailed out the SVB (US). Similarly, the Bank of England has facilitated the sale of SVB (UK) to HSBC, the largest bank in Europe. Customers of SVB in the US and UK can use their bank accounts and deposits as usual.

What is the call to action for banks?

This series of events calls for central banks, CFOs, treasurers, and PR leaders to evaluate their risk management protocols. The following actions are critical going forward for all banks in the world:

- Subject all risk siloes to stress testing: To relate their strategic planning process to the organizational risk and balance sheet silos, banks urgently need to develop their capacity for balance sheet modelling, stress testing, and scenario analysis. Furthermore, reverse stress testing (i.e., figuring out what it will take to "collapse the bank") will compel institutions to have a deeper comprehension of the connections and correlations across various risk types.

- Re-assess how quickly liquidity can be turned to cash: This incident should motivate banks to stress test their contingency liquidity plans and asset monetization assumptions in their liquidity stress testing methodology (i.e., the capacity to convert HQLA buffer into cash and the broader consequences of doing so). To help raise liquidity during times of crisis without turning to a fire sale of assets, treasurers and CFOs should a) examine their liquidity options and b) work to further strengthen their securities financing capacity. Granular announcements on liquidity can reassure investors if they can be made swiftly (while general statements should be avoided.)

- Re-evaluate the concentration risk in the deposit: Banks must evaluate the concentration risk (across sectors, regions, and themes) in their deposit portfolios and, as a result, challenge net liquidity outflow assumptions more vehemently during periods of market stress. In addition to immediate depositors, banks also need to be aware of and take appropriate action in response to the influence of important stakeholders (who are not part of the direct depositor base), mainly when the business is concentrated in a relatively small number of distinct industries or regions.

- Develop a crisis response strategy for the social media era: Banks must create, review, and routinely practice their liquidity crisis playbooks. Banks should frequently hold drills to guarantee a coordinated reaction across siloed and currently unprepared areas of the bank in the case of a similar disaster.

Even for banks with client profiles that are different from SVB's, the crisis serves as a reminder to improve risk management strategies and get ready to respond to crises in a well-planned and tried manner.

{kind=link}