Life insurance, property insurance, travel insurance, health insurance, are just some of the different types of insurance policies and coverages that have emerged since the concept of insurance was first introduced into financial systems. Insurance, which is a more sophisticated form of savings, helps individuals or households deal with major financial shocks/losses, smooth consumption and bounce back from these losses by compensating the insured.

Health insurance for instance covers medical costs for the insured, reducing or even totally eliminating the out-of-pocket costs of health-related expenses, are a significant barrier to accessing quality healthcare. This enables the insured to deal better with emergencies and bounce back without incurring significant costs that may lead to debts.

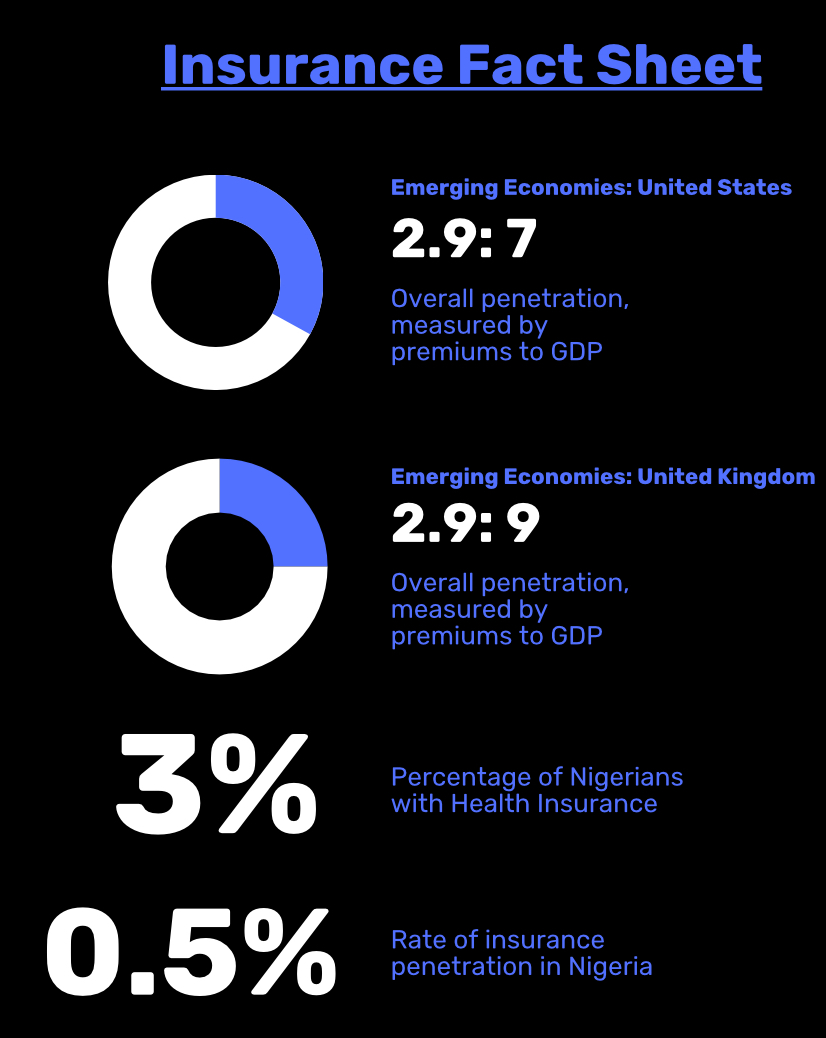

In the face of global and local financial crises, financial risk management technologies like insurance are imperative. However, despite the global knowledge and adoption of insurance, developing countries who are more susceptible to such shocks, have merely trailed behind in the utilization of insurance. For instance, Nigeria which is the largest African country by population has only 0.5% of its over 200 million people insured.

Source: World Bank, Leadway

The low insurance penetration is not baseless, it is often traced to a mix of factors including low income, lack of understanding of the concept, and imperfect information about the insured. This mix of unpleasant factors dissuade players in the industry and also lead to low adoption from the client-side. Thankfully, in recent years research and innovation has led to the evolution of microinsurance, especially for the context of developing economies.

The Opportunity of Microinsurance

EFInA defines micro insurance as insurance services offered primarily to clients with low income and limited access to mainstream insurance services and other means of effectively coping with risk. This scenario holds especially true for many households in developing countries.

Several existing micro insurance efforts in Africa and other developing regions have primarily targeted farmers, offering index insurance, drought insurance, etc. This approach can be introduced into health insurance, given that many households in developing countries like Nigeria face health-related shocks that could permanently affect income and future livelihood.

Micro health insurance is simply the offering of low to medium scale health insurance coverings to low-income people. It is an important piece of the development puzzle because it enhances access to vital healthcare services including access to qualified health personnel and medicines. It is also a powerful tool for expanding Universal Health Coverage (UHC) in developing countries given its potential to improve the poor’s access to quality health services without facing financial hardship as it significantly reduces the out-of-pocket costs for accessing healthcare.

The ‘micro’ nature of microinsurance, makes it target specific and particular shocks. For instance, instead of a comprehensive insurance coverage for a farm, a micro insurance policy may cover only rainfall shocks beyond a certain threshold. This can be especially valuable in healthcare, providing an opportunity for micro insurance policies to cover specific events like emergencies, child births, emergencies, etc.

Microinsurance’s simplified and specific model can also help insurers to tackle the product-understanding gap, as it would be easier to explain the insurance process for a specific (or relatively small) set of events. This will also help insurers to better market micro health insurance products.

Most importantly, microinsurance addresses the low income challenge since it targets low-income people. With premiums priced at low prices, individuals may be more given to purchasing insurance. Additionally, private sector employers in both white and blue collar sectors might more readily purchase these for employees, as a way to improve talent-attraction.

Clusters of Impact

Nearly every part of healthcare can tap into the potential of micro health insurance to improve access to quality healthcare. We highlight three high priority especially in the context of developing countries that can leapfrog overall health outcomes.

Maternal Care

Maternal mortality remains a major health issue for many women in developing countries. From 2017-2020 alone, Nigeria’s maternal mortality rate rose by approximately 17%.

While there are a mix of factors at play, the rising cost of healthcare is an important factor dissuading women from engaging skilled birth attendants from conception until delivery, which has led to many avoidable deaths.

Micro health insurance presents an opportunity to tackle this health crisis, either by covering in part or full the medical expenses associated with childbirth, or by innovative pooling of resources that can target women groups.

Accidents & Emergency Care

Infrastructural and development deficiencies increase the propensity for accidents, including road and work-related accidents. In addition, to accidents, health emergencies such as cardiac arrests, etc. also continue to claim lives. Accidents and emergencies also financially destabilize households in the long term, especially if the breadwinner is affected. Micro health insurance covers tailored to this area is extremely valuable.

Mental Health Care

In the developing world, mental health issues tend to be viewed as irrelevant, this alongside financial constraints makes it difficult for people to pay for mental health issues. Micro insurance covers that target this area can take off the financial decision burden from the insured, enabling them to access the required care with zero out-of-pocket cost.

The Time is Right

EFInA’s Access to Financial Services in Nigeria Survey (2016), spotlights that 32.1 million Nigerian adults are interested in using microinsurance products. As the country’s young adult population keeps growing, this number is expected to have increased at least by 5% in the past 8 years since the survey.

The growth and maturity of Nigeria’s financial services sector also poises the country for this innovation. Insurance companies can partner with fintech players to drive marketing and sales of micro health insurance packages.

As economic hardship bites especially in developing countries, micro health insurance can open up access to quality and urgent healthcare for many, especially the middle-class, the poor and the underserved who bear the brunt of out-of-pocket health expenses.

What Next?

Adverse health events happen to everyone, this is the notion behind classical health insurance. But when these adverse events happen to the poor, it can disproportionately affect their livelihoods afterwards, this is the notion behind micro health insurance. The opportunity of micro health insurance lies in its ability to improve access to healthcare for the poor, especially in developing countries.

Governments, policy makers, insurance companies, donor organizations can tap into this opportunity to improve health outcomes, expand universal health coverage and deepen the penetration of the insurance market in developing countries.

A few opportunities to explore include:

- Governments and policy makers can integrate micro health insurance packages into benefits packages for staff.

- Private employers of labor and policy makers who cannot cover classic health insurance for staff, should adopt at least micro health insurance coverages.

- New and existing players in the insurance and microinsurance industries need to develop more innovative micro health insurance products that meet the needs of

- Donors should prioritize funding startups and projects seeking to build micro health insurance products and innovations.

- Partnerships to expand the reach of micro health insurance should be prioritized as collaborations can open new markets. It can also create network efficiencies.

{kind=link}