Stakeholders have formulated policies to mainstream financial inclusion into all aspects of human lives. Funding has been disbursed to necessary corners to ensure that adequate research, advocacy, and implementation become accessible and sustainable. This decade could as well be tagged the decade of financial inclusion.

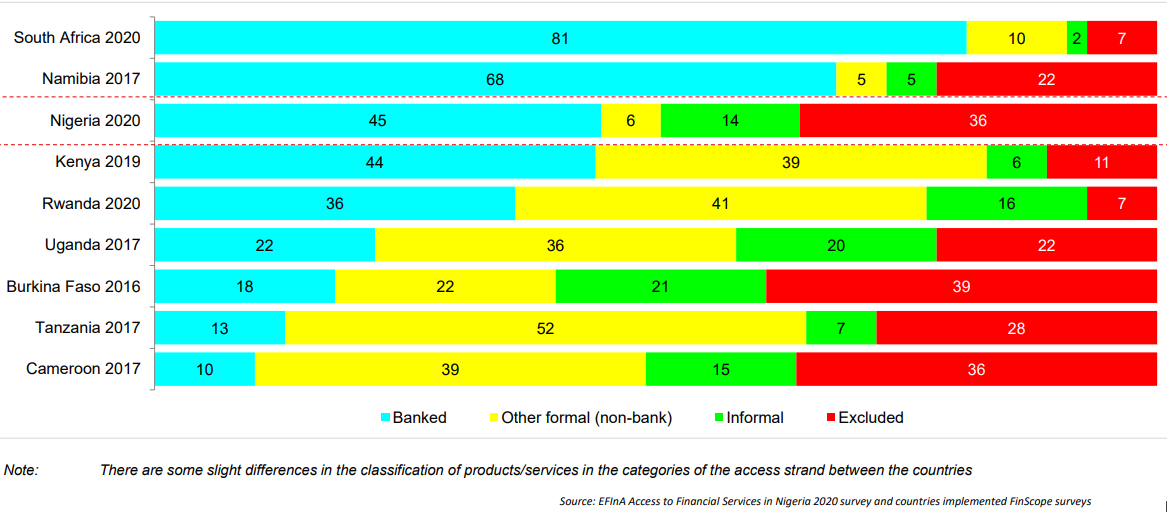

However, financial exclusion remains a perplexing reality in Nigeria. In the recent Enhancing Financial Innovation & Access (EFInA) report, 36% of Nigerian adults or 38 million adults remain completely financially excluded. That is high compared to other African countries, as seen in the image below.

While the benefits of financial inclusion are widely known, there are still a significant number of people in Nigeria whose daily operations escape the shining light of financial empowerment and liberation. Financial inclusion as a concept is not limited to owning bank accounts or making payments but extended to pension and insurance but in the context of today’s musing, I would dwell more on accessibility to digital financial services.

In 2020, I imagined a situation where I have no access to digital financial services (debit cards, USSD and mobile banking). While it seems almost impossible, I decided to operationalise the concept of alpha-testing on financial inclusion by stripping my primary savings account of anything digital.

I put all my monies in a savings account with no digital footprint whatsoever. This means that I would have to go into a physical bank, queue, and withdraw cash whenever I needed money. This experiment translated into long hours in banking halls, productive hours wasted, unnecessary hassle with other customers, increased risk of contracting COVID-19.

According to the Financial Insights from Kantar, a majority of poor, rural and less-educated persons are financially off-grid. To the majority, it is simply not having a bank account; for many, it is not having physical access to a bank, and for some, it is not having access to digital financial services. Either of these three situations scream exclusion.

My self-induced exclusion lasted for two months. Two months of increased stress, reduced productivity and possible health implications. Yet all these pale compared to what wholly excluded persons face every day—no access to digital financial services, no credit history and, most importantly, no access to financing.

Financial exclusion is an acute deprivation – one that no human should experience.

{kind=link}