Alliances, partnerships, policies, regulations, and credit facilities, among others, have been employed and given in the push for the adoption of formal and digital financial services for financial inclusion in Africa. The interoperability of a national payment switch for frictionless transactions within, outside of, and across borders remains a germane issue. Foundational to the implementation of an interoperable payment system is a switch network. Therefore, a switching system is essential for achieving seamless payments at the regional, national, and international levels.

Most recently (March 23, 2023), the Board of Directors of the African Development Bank and São Tomé and Príncipe’s government signed a $3.2 million agreement for the upgrade of the nation’s payment switch system. This loan which will be disbursed through Nigerian Trust Fund comes as a supplement to the African Development Fund grant of $2 million made in 2017 to support Sao Tome and Principe with a state-of-the-art Automatic Transfer System (ATS+). Specifically, the upgrade will allow for automatic Real Time Gross Settlement (RTGS) modules and Automated Clearing House functionalities, strengthening the clearing and settlement of payments.

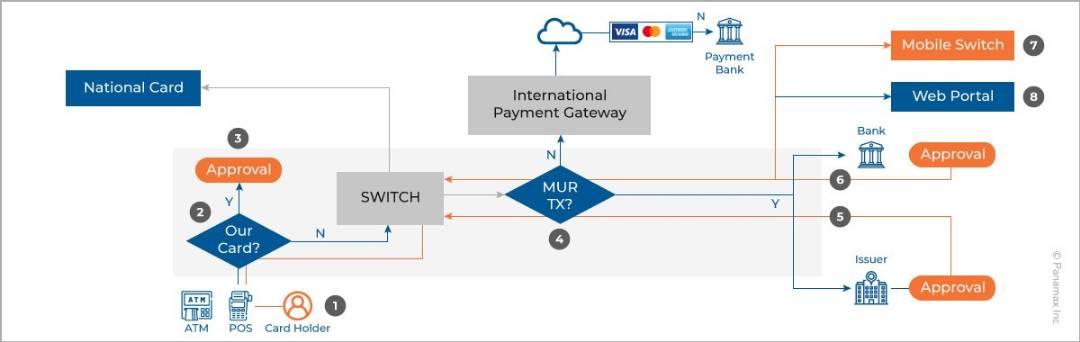

What is a Payment Switch?

A Payment Switch is a type of electronic payment network that facilitates the processing of transactions between different financial institutions, such as banks or credit card companies.

[Source: Manasi Mulasi, October 6, 2020. Reimagining Payments through National Payment Switch. Available at https://bit.ly/3KnB8Qb.]

A payment switch typically operates as an intermediary or bridge between the merchant acquiring bank (the bank that accepts the payment on behalf of the merchant) and the card issuing bank (the bank that issued the payment card to the customer) and the customer. When a customer makes a payment using their card at a merchant, the transaction details are sent to the switch payment system, which then verifies the transaction with the card issuer and processes the payment.

Payment switches are often used for ATM transactions, debit card transactions, and other types of electronic payments. They are designed to handle large volumes of transactions quickly and securely, while also ensuring that funds are transferred correctly between the different parties involved.

Status of São Tomé and Príncipe’s National Payment System

According to a report by First Initiative, São Tomé, and Principe's payment infrastructure is underdeveloped and unable to handle domestic or foreign retail transactions or interbank payments in a secure and timely manner. As a result, both retail and interbank transfers are challenging and expensive, and cash is still widely used.

The current payment system infrastructure in the nation consists of two components:

- a card switch run by SPAUT, a joint venture of São Tomé and Príncipe’s Central Bank (BCSTP), commercial banks, and telecommunications companies; and

- a manual cheque clearing system (SICOI) run by So Tomé and Prncipe's Central Bank (BCSTP), which requires the physical exchange of cheques and involves many manual processes, making the system inefficient and generally prone to errors.

The U.S. Department of State - Bureau of Consular Affairs in its travel information as of March 2023, notes that Sao Tomean Dobra must be purchased from travelers using their own money. Only a small selection of foreign currencies are accepted by banks for conversion. Local banks, however, can only issue domestic debit cards which are accepted at São Tomé and Príncipe’s ATMs; they are unable to issue international cards, which promotes the use of cash and restricts business operations. Many international hotels have forged a partnership with an overseas bank to take foreign credit cards to cater to tourists and other visitors.

When compared with similar climes such as Mozambique, São Tomé and Príncipe seems to be grappling. Since after a a five day blackout of the Interbank Bank of Mozambique’s network in 2018, Mozambique has since made significant strides to improve its payment system including the launch of a new digital payment solution, in 2020. This solution was launched and integrated with Mozambique’s payment system, Sociedade Interbancária de Moçambique (SIMO) to unify all electronic payment platforms in Mozambique, including the implementation of interoperability between digital money institutions, as well as improve international transfers.

The abysmal state of Sao Tome's payment system has necessitated the . To this end, BSCTP continues to request multilateral assistance.

What Makes a National Payment Switch or its Upgrade Beneficial?

A Payment Switch is essential to advancing financial inclusion because it strengthens electronic payment services for the included as well as provides electronic payment services to the formally excluded (those without access to conventional banking services).

Some benefits of a National Payment Switch include:

- Interoperability and Attraction to New Players: A national payment switch would strengthen the effectiveness and efficiency of digital payments but also facilitate the entry of new financial service providers, by enabling interoperability between different payment systems and financial institutions

- Increased Access to Financial Services: NPS can help expand the reach of financial services to underserved and unbanked populations, particularly in rural and remote areas. The switch system offers a platform through which users can access digital banking services, such as the ability to transfer money, withdraw money, and make electronic payments.

- Increased Efficiency: NPS can aid the efficiency of financial transactions by enabling real-time processing and settlement of transactions. This reduces the time and costs associated with manual processes and paper-based transactions, making financial services more accessible to people who are financially excluded.

- Lower Transaction Costs and Security: The use of electronic payments can reduce costs and risks related to managing cash, such as transportation, theft, fraud, and loss. Generally speaking, electronic payments are more affordable and safe than cash-based ones. Switch payment systems may help to further reduce transaction costs, increasing the affordability and accessibility of financial services for those who are monetarily excluded. Additionally, NPS offers a secure platform for transaction handling that includes authentication procedures and encryption protocols to fend off fraud and other security risks.

- Improved Data Collection: NPS can help to improve data collection on financial transactions, enabling financial institutions to better understand the needs and behaviors of their customers Furthermore. accurate data collection makes it possible to acquire and report gender-disaggregated data. This can help to inform human-centered development and design of new financial products and services that meet the needs of underserved and unbanked populations.

In conclusion, it is important to note that the AFDB's support would provide a partial fix to Sao Tome and Principe's national payment switch - as RTGS and ACH upgrade does not include instant payments like TIPS in Tanzania or PayShap in South Africa. Therefore, there is more work to be done. Regardless, this is a step in the right direction.

{kind=link}